2026 Nigeria

Macroeconomic Outlook

The Nigeria Macroeconomic Outlook 2026 examines the global and domestic economic environment, analyzing key reforms, fiscal trends, and projections that will shape Nigeria’s economic performance in the year ahead. Despite global uncertainty, Nigeria’s economy shows signs of resilience driven by structural reforms, improved fiscal management, and stability in the foreign exchange market.

Global Economic Outlook

The Global Economy faced significant headwinds in 2025, driven by high levels of uncertainty in trade relations.

Global growth and trade volumes are projected to weaken in 2026 amid rising tariffs, policy uncertainty, and supply disruptions.

Inflation eased globally to an average of 4.2% in 2025, but wide gaps persist.

Advanced economies have largely stabilised prices, while many developing countries still face double-digit inflation due to currency weakness and structural challenges.

Monetary Policy Developments

From the US Federal Reserve’s cautious rate cuts to Nigeria’s gradual policy shift, central banks adopted different approaches to navigate easing inflation and slowing growth in 2025.

Base Interest Rate Adjustments,

January–September 2025

Despite a $500 billion trade growth in early 2025,

renewed tariff threats and geopolitical conflicts cloud the horizon for 2026, with forecasts falling to just 0.5%.

Nigeria’s 2025 Economic Performance

Nigeria’s economy continued its reform-driven recovery in 2025, supported by FX unification, stable monetary policy, and a resilient services sector.

Sectoral Contribution to GDP

(Q2 2025)

Services remain Nigeria’s growth engine, while agriculture continues to recover.

Inflation, Monetary & Fiscal Policy

Inflation showed signs of moderation in 2025, enabling cautious policy easing by the CBN while fiscal reforms aimed to improve revenue efficiency.

Trade Surplus Strengthens as Naira Stabilizes

Nigeria recorded another year of positive trade balance in 2025, driven by strong crude exports and a more transparent FX regime. The Naira held steady between ₦1,450–₦1,650 per dollar, a stark contrast to 2024’s volatility.

Outlook for the Domestic Economy

Veriv Africa’s 2026 outlook builds on advanced econometric forecasting combining ARIMA and VAR models to simulate Nigeria’s macroeconomic performance under varying domestic and global conditions.

This is the bull case. It is quite optimistic relative to the base case.

This represents the business-as-usual scenario. It assumes the basic ceteris paribus (all things equal) principle, that the macroeconomic condition remains largely the same with no significant changes.

This is slightly pessimistic compared to the base case, representing the bear market scenario.

$40 Billion Flows Back Into Oil and Gas

2025 marked a decisive rebound for Nigeria’s oil and gas sector. Improved fiscal terms and stronger confidence in reforms attracted over $40 billion in new investments across 79 Field Development Plans (FDPs), the highest in a decade.

Electricity Market Development

The decentralisation wave reshaped Nigeria’s electricity landscape in 2025. Following the Electricity Act 2023, 19 states now regulate their own power markets expanding autonomy, competition, and private investment.

The grid-connected generation capacity edged up to 5,395 MW, driven by gas and hydro contributions.

Yet, weak billing and collection systems cost the industry over ₦158 billion in just one quarter.

Non-Oil Exports Grow 19%, Cocoa Leads the Way

Nigeria’s diversification story gained traction in 2025. Non-oil exports rose by 19% year-on-year to $3.23 billion in the first half of the year the highest in recent history.

The non-oil sector continued its positive run in the first half of 2025,

with total export earnings of $3.225 billion in the first half of 2025, compared with $2.7 billion in the first half of 2024.

Risks to the Outlook

As Nigeria looks toward 2026, multiple headwinds threaten its steady economic recovery. While progress has been made in exchange rate stability, inflation control, and debt management, the economy remains highly exposed to oil dependence, global volatility, and structural inefficiencies.

Potential Global Economic Slowdowns

The global economy has largely avoided a worldwide recession, showing significant resilience despite repeated attacks on trade relations by key global economies.

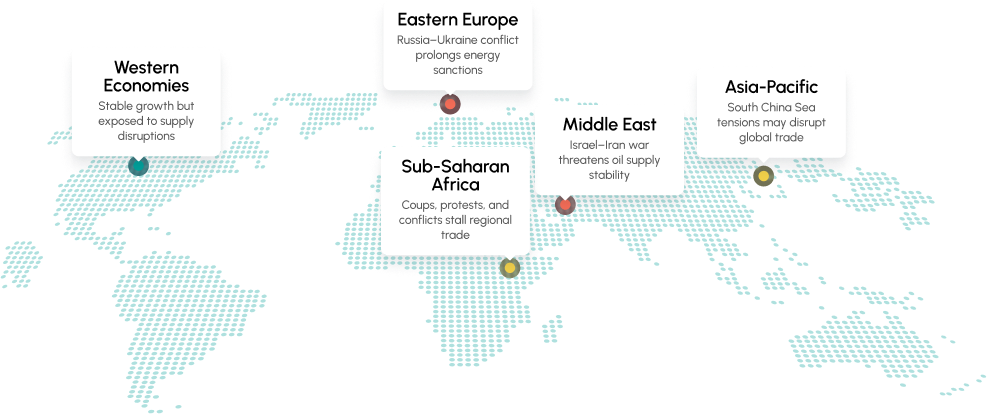

Geopolitical Risks and Their Impact

The global economy in 2025 was shaped by conflict, fragile diplomacy and shifting alliances. From the Middle East to Africa, tensions continued to disrupt trade flows, energy security, and investor confidence. As nations navigate wars, sanctions, and fragile peace deals, global growth risks remain elevated going into 2026.

Labour Market and Employment Risks

Nigeria’s labour market struggles persist, driven by weak linkages and limited formal opportunities, as underemployment and informality dominate the economy, multiple taxation and entry barriers stifle MSMEs, weak labour protections leave informal workers vulnerable, and the absence of social safety nets continues to limit productivity and overall welfare.

Fiscal Consolidation Strategies

Sustaining Nigeria’s fiscal health requires more than short-term revenue adjustments, it demands deep institutional reforms and strategic investment in sectors that can diversify government income. Strengthening tax systems, improving transparency across MDAs, and enforcing accountability frameworks will help reduce leakages and improve fiscal discipline.

Monetary Policy Adjustments

Nigeria’s monetary environment remains tight despite a minor policy rate cut, balancing the need to control inflation with the need to stimulate growth. While the elevated MPR continues to support foreign exchange stability, it suppresses borrowing and investment highlighting the urgency for a gradual, coordinated shift toward a more growth-accommodative stance as inflation moderates.

The MPR was reduced by 50 basis points to 27%, yet it remains one of the highest interest rate levels in over a decade and continues to sustain high borrowing costs despite its short-term FX benefits.

Structural Reforms

Nigeria’s reform agenda is expanding across tax, energy, and financial systems, but deep structural bottlenecks continue to limit the impact of these changes. Addressing bureaucracy, unlocking the power of the informal sector, and strengthening export competitiveness will define how quickly the economy can transition into a productivity-driven and investment-ready environment.

Labour Market & Employment Policy Recommendations

Nigeria’s labour market can unlock massive productivity gains by equipping workers with relevant skills, enforcing stronger labour protections, and creating an investment-ready environment for job-intensive industries. Targeting youth employment, formalisation, and sector-specific capacity building will be central to reducing unemployment and improving economic resilience.

Encouraging private investment especially

in decentralised energy systems will boost reliability for households and industries while reducing pressure on the national grid.

Veriv Africa Deal Book

A curated shortlist of high-value opportunities across Nigeria’s most promising sectors. Each pick reflects strong market fundamentals, policy tailwinds, and attractive risk-adjusted returns for forward-looking investors.

Lithium Mining Industry

Nigeria’s lithium belt is emerging as a high-potential asset class, powered by global EV demand and domestic reforms aimed at diversifying away from crude oil.

Global lithium market projected to reach $74B by 2030 at 18% CAGR.

Key Opportunities and Potential Structure

There is a rising global demand for lithium, driven by electric vehicles and battery storage. Nigeria has been pushing mining-sector reforms: streamlined licensing, Solid Minerals Development Fund, and the new Nigerian Solid Minerals Corporation. Major opportunity gaps: exploration data, artisanal dominance, and high-value beneficiation are still underdeveloped.

Nigeria’s lithium sector has strong potential

but faces risks such as insecurity, illegal mining, currency and political volatility, and community resistance. These risks can be managed with proper mitigation plans.

Nigerian Electricity Sector

Following the Electricity Act 2023, Nigeria’s power sector has opened up for state-level regulation creating unprecedented entry points across generation, transmission, and distribution.

Key Opportunities and Potential Structure

Half of Nigeria’s 200M population still lacks reliable electricity. States now control pricing, licensing, and incentives enabling targeted investment choices.

Capital requirements range from $15M (small generation) to hundreds of millions (statewide grids).

Nigeria’s electricity sector carries major currency

and political risks, as revenues are earned in naira and regulatory certainty varies widely across states. Investors must factor in these risks when choosing where to operate.

Practical Realities of Investing in Nigeria

The opportunities discussed above, in addition to other opportunities tracked by our team, possess significant potential. However, each intending investor must consider the practical aspects of investing in the Nigerian market. Key factors to consider include:

Tax Changes

Starting January 2026, the corporate tax remains 30%, but the capital gains tax will increase from 10% to 30%, meaning investors need higher returns to achieve previous post-tax gains. Exemptions apply to investments below ₦150 million and reinvestments within a specified period.

Land Tenure

In rural areas, land tenure can be complex. Under the Land Use Act, state governors can allocate land and grant certificates of occupancy for up to 99 years, while the federal government regulates mining licenses. Mining projects must navigate both state and federal approvals, as well as local community interests.

Security

Nigeria faces security challenges such as kidnapping, banditry, illegal mining, and terrorism, especially in key food and mining regions. Investors can arrange protections with state and security agencies, but comprehensive insurance is still essential.

Political & Regulatory Risks

Beyond insecurity, political risks are significant for investors, especially in mining, including bans on operations or mineral exports and new government laws promoting local value addition. Conflicts may arise with state governors over taxation or environmental issues, making collaboration with local consultants and legal advisors essential.